US Treasury Yield Curve

How do you interpret the Yield Curve?

A yield curve chart shows how much money you can make by investing in government bonds for different lengths of time. Normally, the longer you invest, the more money you make. So the line on the chart goes up as the time gets longer.

When the line goes down this is called an inverted yield curve. It happens when short-term bonds pay more money than long-term bonds. This may imply a negative view of the economy and a sign of a recession upcoming.

Invest in Treasury Bills (T-bills) and earn a -%* yield

Earn a higher yield than a high-yield savings account**

Normal vs Inverted Curve

An inverted yield curve occurs when long-term yield rates are lower than short-term rates and is often a precursor to a recession, having preceded nearly all recessions since 1960 by about a year.

Financial markets can be impacted by inverted yield curves. During times of economic turbulence, investors may flock to purchase longer-dated bonds if they anticipate interest rates falling over the short term due to the Fed lowering rates to combat economic weakness.

A normal yield curve shows higher rates for long-term bonds, which generally indicates confidence in the economy.

An upward-sloping yield predicts higher interest rates across financial markets. The normal yield curve is considered more robust in predicting market conditions compared to other market indicators and variables by financial analysts.

How does the Treasury yield work?

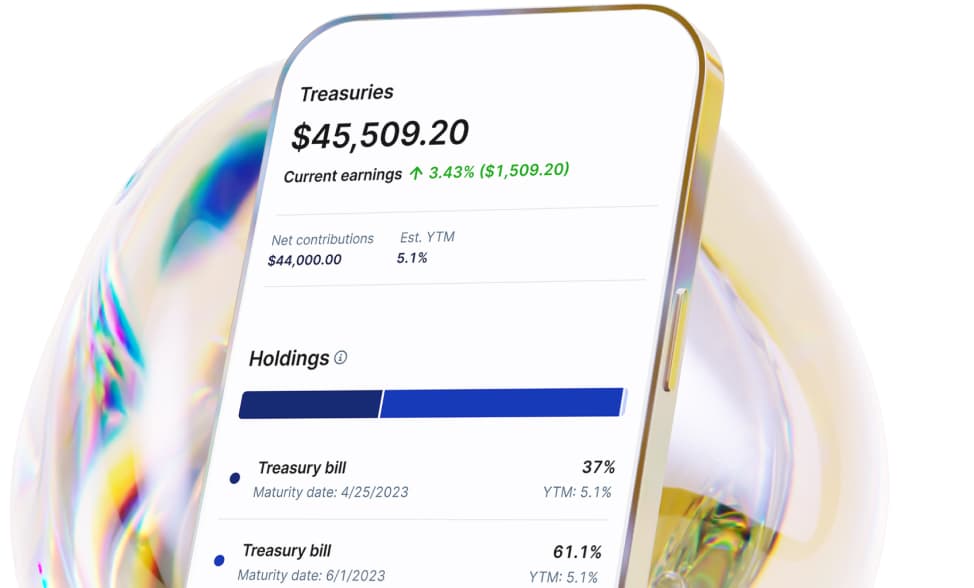

5% annualized yield on $1,000 over a period of 6 months is $25. Because Treasury bills are purchased at a discount to their face value, you’ll pay about $975. Then, when they reach maturity after 6 months, you’ll get the full $1,000, netting you a $25 profit.

Importance of the Treasury yield curve

The US Treasury yield curve is a visual representation that displays the interest rates of US government bonds based on the length of time until they mature.

By plotting the yields against different maturities, the graph allows individuals to understand the amount of interest the government must pay back for various time frames and also gives insight into the government's borrowing plans.

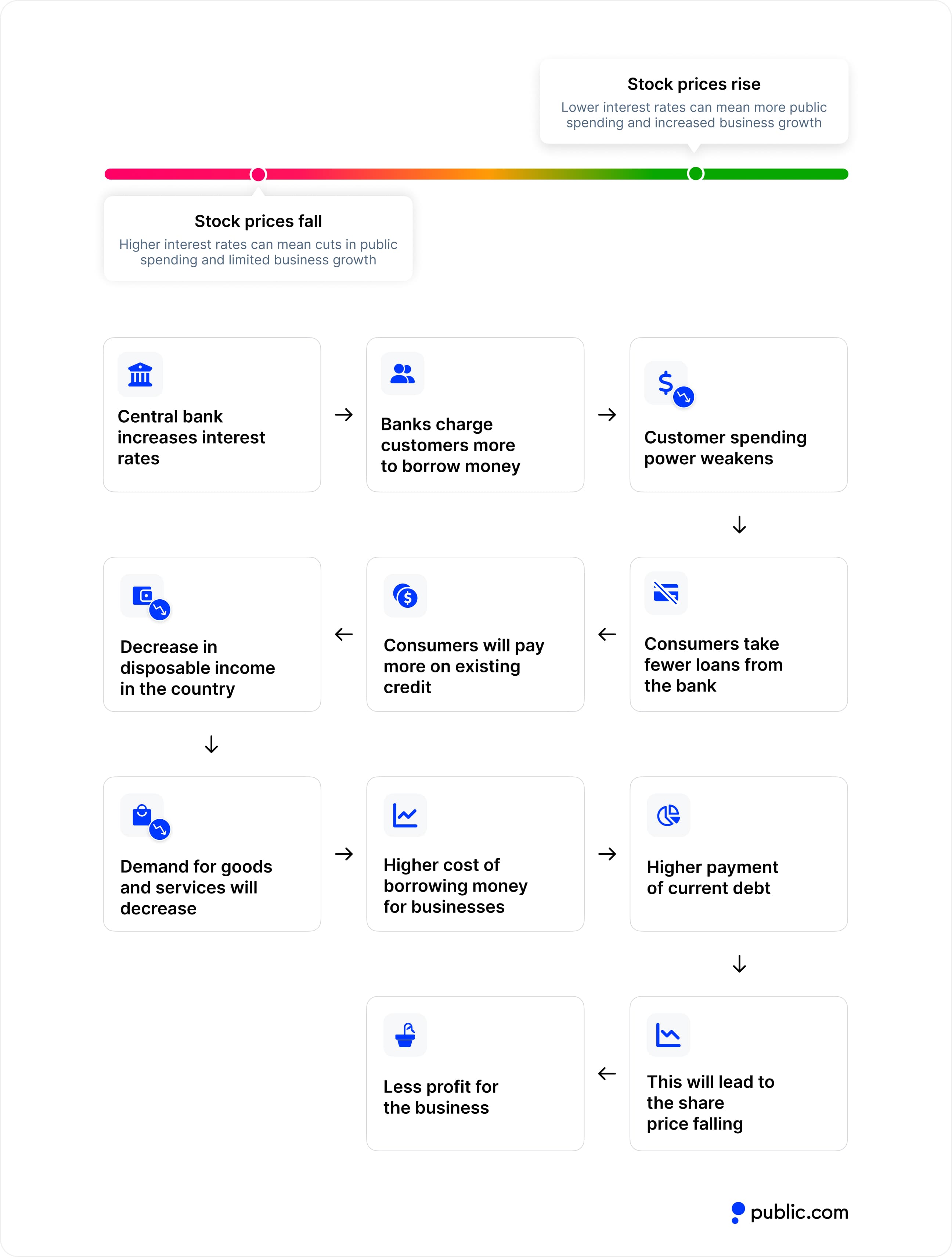

How Interest rates affect stock market

The relationship between interest rates and stocks is generally inverse. While changes in interest rates may take time to manifest throughout the economy, stock market movements are prompt in response. The reason for this is that interest rate fluctuations alter the value of a future dollar, which impacts the current value of a company’s future profits. In a rising rate environment, future dollars are worth less and in turn, future profits are worth less, so today’s company value must decline to reflect that drop in future value. This decline is not because the company is doing worse, but solely because interest rates have changed.

The reason for this is that interest rate fluctuations alter the value of a future dollar, which impacts the current value of a company’s future profits. In a rising rate environment, future dollars are worth less and in turn, future profits are worth less, so today’s company value must decline to reflect that drop in future value. This decline is not because the company is doing worse, but solely because interest rates have changed.

A rise in interest rates means a reduction in spending power for consumers. The higher credit rates discourage consumers from taking loans with their limited funds and they often must pay more on existing debt. This trickles down to businesses where the cost of borrowing becomes more expensive, including higher debt repayments. This shift in repayment plans leads to decreased profit, lower investment spending, and potentially lower stock prices as a result. The faster and more aggressive the rate increases, the more impact they will have on these factors.

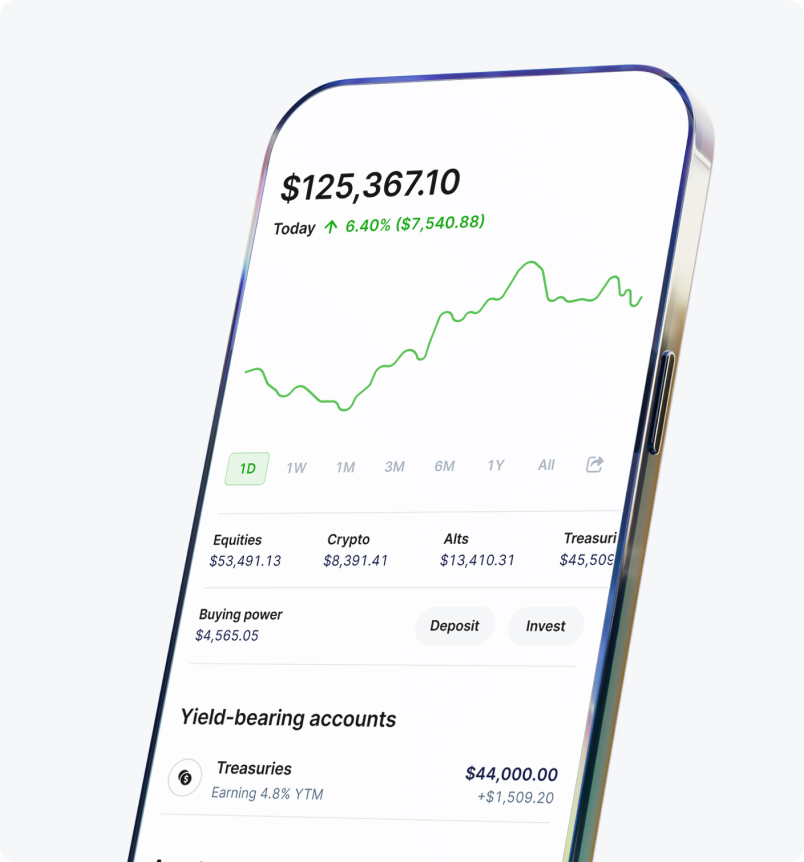

How to buy T-Bills with Public

Move your savings

It’s easy to transfer your savings to Public by linking a bank account or making a deposit with your debit card.

Create your Treasury Account

Once you’ve moved your savings, you can purchase and manage your Treasury bills from one account.

Lock in your rate

Treasury bills are a fixed-income asset, which means their rate of return is fixed at the time of purchase.***

Historic Treasury Bill Rates

Earn a -%* yield

* Rate is gross of fees. T-bills are purchased in increments of $100 par value at a discount; any remaining balance after purchase is held in cash. Risks.

** Public is not responsible for the accuracy, timeliness, or completeness of information on third-party websites. Open to the Public Investing is not a bank and does not offer savings accounts. You should contact your bank for current and complete information about available account types, including applicable interest rates. Risks.

*** Rate of return is annualized and assumes holding T-bill until maturity.